Outpacing Inflation with Stocks

Inflation is back in the news of late, as the year-over-year change in the consumer price index is at the highest level since 2023 in the US which is the worlds largest economy. This may stoke fears of further inflation for many investors.

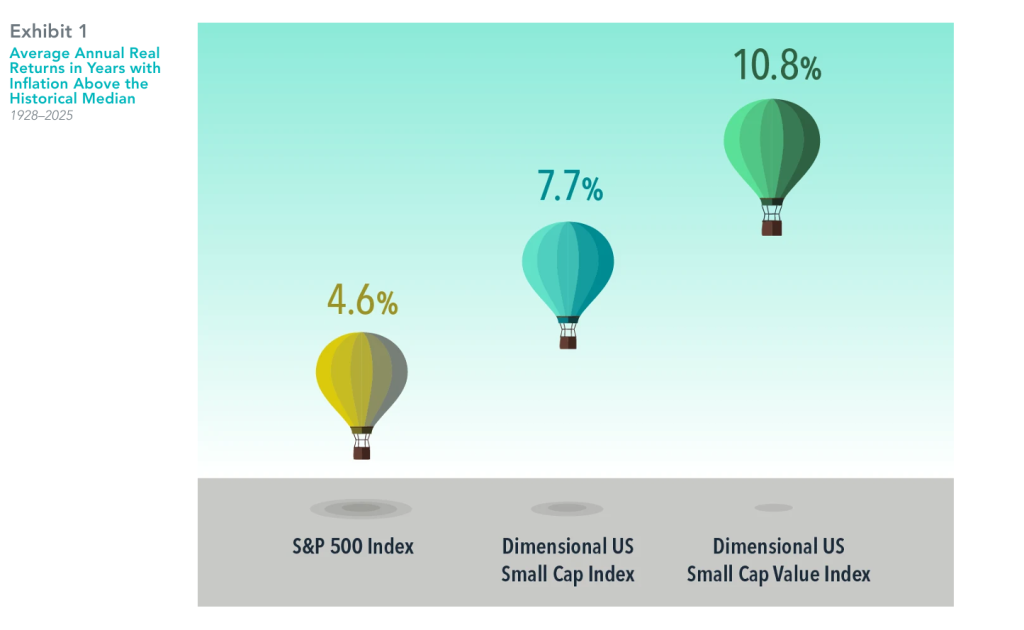

It’s important to note that expected inflation is incorporated into the expected returns demanded by market participants. To the extent inflation is expected to impact either future cash flows from an investment, or the discount rate applied to these cash flows, market prices adjust to compensate, resulting in positive expected real returns. This is borne out in historical data. Average real returns for the broad US stock market, based on the S&P 500 Index, have been positive even in years when US inflation was above the historical median. Average real returns for US small cap and small cap value stocks have been even higher, implying investors should not shy away from tilting toward higher expected return stocks even if inflation expectations are elevated.

We believe one way for investors to deal with inflation is to outpace it. Stocks have been a good way to do this historically, as the evidence from the US illustrates.

To review the diversification of your own investments feel free to get in touch.

In USD. US inflation is the annual rate of change in the consumer price index for all urban consumers (CPI-U, not seasonally adjusted) from the US Bureau of Labor Statistics. Nominal return is the rate of return on an investment without adjusting for inflation. Real return is the rate of return on an investment after adjusting for inflation. Real returns are calculated using the following method: [(1 + nominal return) / (1 + inflation rate)] – 1. The Dimensional indices represent academic concepts that may be used in portfolio construction and are not available for direct investment or for use as a benchmark. Index returns are not representative of actual portfolios and do not reflect costs and fees associated with an actual investment.

See “Index Descriptions” in the appendix for descriptions of the Dimensional index data.

S&P data © 2026 S&P Dow Jones Indices LLC, a division of S&P Global. Indices are not available for direct investment.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

Key steps to take before the tax year ends

With the 2025/26 tax year-end approaching, now is the time to act to maximise your financial opportunities. Key priorities include using your £20,000 ISA allowance for tax-efficient growth and contributing up to £60,000 (or more if carry forward is available and relevant earnings are sufficient) to your pension to take advantage of tax relief and long-term benefits. Other allowances, such as Capital Gains Tax, Dividend Allowance and Junior ISAs, are ‘use it or lose it’ opportunities. On page 08, we explain why early action avoids last-minute stress, secures tax savings and ensures financial growth.

With rising life expectancy, more of us will need long-term care, making early financial planning essential. Fees have surged, and regional cost disparities add to the challenge. Funding options include annuities, insurance, investments and equity release. On page 12, we consider how professional advice is crucial for navigating tax implications and securing a sustainable plan for future care needs.

Inheriting wealth can be life-changing but comes with challenges. On page 28, we explain why holding excessive cash may not be the best choice as inflation erodes its value. Instead, consider diversified investments to foster growth. Align your strategies with your goals, whether it’s retirement or supporting your family, and seek professional advice to maximise tax benefits and avoid pitfalls.

Financial uncertainty is growing, with many feeling life is unpredictable. Rising inflation, energy costs, and tax increases fuel concerns, prompting shifts such as increased cash savings and delayed retirements. While saving is important, balancing short-term needs with long-term investments is key. Reviewing pensions and seeking advice builds resilience and confidence. Turn to page 06.

A complete list of the articles featured in this issue appears opposite page and on page 03.

Wealth planning for your future

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

MARKET INSIGHTS: The Cost of Trying to Time the Market

Considering how dire the headlines and stock price moves appeared to be in April with the Tariff headlines I know it’s tempting to move to the sidelines and delay making investments or even sell and wait and see how things develop with a view to ‘re-entering the market’ when valuations might be more attractive and the outlook clear. The problem is the evidence suggests that approach rarely works out! With new record highs being made in the US stock market last week I thought it’s worth reflecting on this.

The impact of being out of the market for a short time can be profound, as shown by this hypothetical investment in the MSCI World Index, a broad Global stock market benchmark.

- A hypothetical £1,000 investment made in 2015 turns into £3,214 for the 10-year period ending December 31, 2024.

- Miss the MSCI World’s best week, and the value shrinks to £2,940. Miss the best three months, and the total return falls to £2,498.

- There’s no proven way to time the market—targeting the best days or moving to the sidelines to avoid the worst. Staying invested and focused on the long term helps to ensure that you’re in position to capture what the market has to offer.

In GBP. For illustrative purposes. Best performance dates represent end of period (April 08, 2020, for best week; April 14, 2020, for best month; June 18, 2020, for best three months; and September 15, 2020, for best six

months). The missed best consecutive days examples assume that the hypothetical portfolio fully divested its holdings at the end of the day before the missed best consecutive days, held cash for the missed best consecutive days, and reinvested the entire portfolio in the MSCI World Index (net div., GBP) at the end of the missed best consecutive days. Data presented in the growth of £1,000 exhibit is hypothetical and assumes reinvestment of income and no transaction costs or taxes. The data is for illustrative purposes only and is not indicative of any investment. MSCI data © MSCI 2025, all rights reserved.

Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

Market Insight: Sweeping changes

Welcome to our latest issue. The October 2024 Budget proposed sweeping changes to Inheritance Tax (IHT), significantly tightening the laws that were previously more forgiving for families with trading businesses and farmland. Effective from April 2026, these types of assets will now incur IHT at a reduced rate of 20% on valuations exceeding £1 million. On page 04, we consider why the changes are leaving many families scrambling to reassess their estate planning strategies.

Ten years ago, pension freedoms revolutionised how people access their retirement savings. These changes offered savers over 55 greater options to withdraw and manage their pension pots. However, a decade later, research indicates that many individuals are making critical financial decisions without seeking advice or fully understanding the tax implications. Read the full article on page 03.

A complete list of the articles featured in this issue appears on page 02.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below