Key steps to take before the tax year ends

With the 2025/26 tax year-end approaching, now is the time to act to maximise your financial opportunities. Key priorities include using your £20,000 ISA allowance for tax-efficient growth and contributing up to £60,000 (or more if carry forward is available and relevant earnings are sufficient) to your pension to take advantage of tax relief and long-term benefits. Other allowances, such as Capital Gains Tax, Dividend Allowance and Junior ISAs, are ‘use it or lose it’ opportunities. On page 08, we explain why early action avoids last-minute stress, secures tax savings and ensures financial growth.

With rising life expectancy, more of us will need long-term care, making early financial planning essential. Fees have surged, and regional cost disparities add to the challenge. Funding options include annuities, insurance, investments and equity release. On page 12, we consider how professional advice is crucial for navigating tax implications and securing a sustainable plan for future care needs.

Inheriting wealth can be life-changing but comes with challenges. On page 28, we explain why holding excessive cash may not be the best choice as inflation erodes its value. Instead, consider diversified investments to foster growth. Align your strategies with your goals, whether it’s retirement or supporting your family, and seek professional advice to maximise tax benefits and avoid pitfalls.

Financial uncertainty is growing, with many feeling life is unpredictable. Rising inflation, energy costs, and tax increases fuel concerns, prompting shifts such as increased cash savings and delayed retirements. While saving is important, balancing short-term needs with long-term investments is key. Reviewing pensions and seeking advice builds resilience and confidence. Turn to page 06.

A complete list of the articles featured in this issue appears opposite page and on page 03.

Wealth planning for your future

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

Mind the Gap - Diversifying Across Countries

While many of us enjoy an international holiday this summer it might be timely to talk about countries!

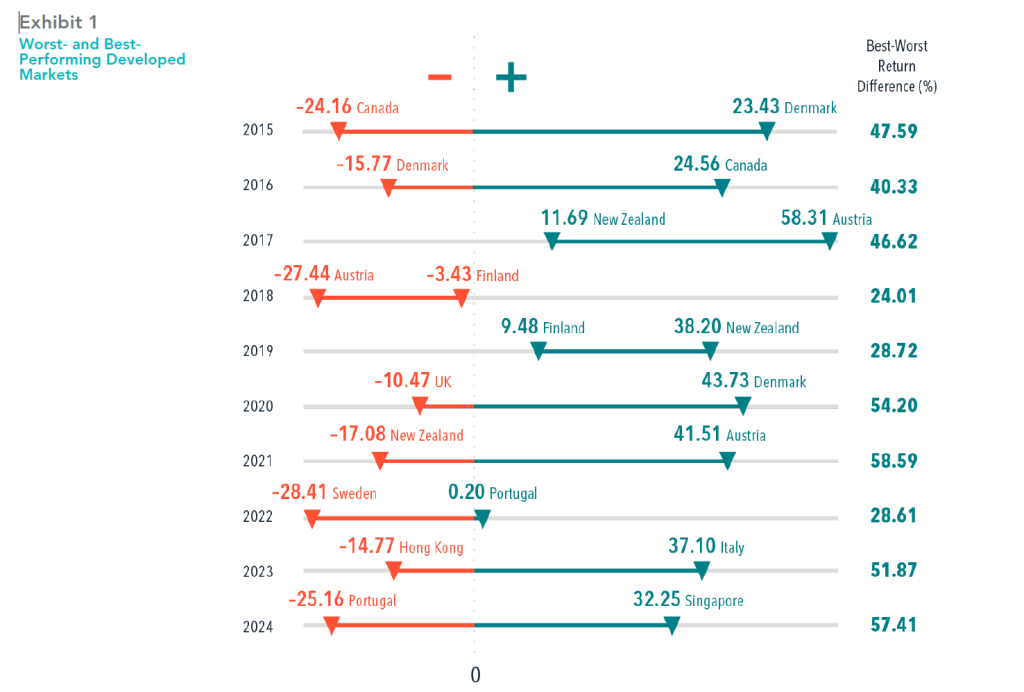

Recently, there’s been a lot of noise around which country one should invest their savings in for the best growth, and the idea of allocating away from the US for many reasons. In the first half of 2025, developed markets outside the US returned 19.0%, outperforming the US and emerging markets. But that outcome masks the wide range of returns across individual countries, from Spain’s 43.0% to Denmark at −5.5%. This kind of dispersion isn’t unusual—it’s a defining characteristic of global investing.

On average, the difference in return between the best- and worst-performing country

exceeded 43% over the past 10 calendar years. It’s no wonder investors may be tempted to chase recent winners or try to avoid losers. However, there’s little evidence that timing strategies consistently pay off. Country returns can turn quickly. For example, Canada posted the worst returns in 2015, down over 24%, but was the top performer in 2016, up over 24%. An investor who lost patience at the end of 2015 potentially missed out on the subsequent market recovery.

Country volatility is a normal part of global investing. Fortunately, as 2025 illustrates,

investors in a globally diversified portfolio can benefit from international diversification

without risking getting on the wrong side of country swings.

In USD. The US is included in the developed markets analysis. MSCI data © MSCI 2025, all rights reserved. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio. Diversification neither assures a profit nor guarantees against a loss in a declining market.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

MARKET INSIGHTS: The Cost of Trying to Time the Market

Considering how dire the headlines and stock price moves appeared to be in April with the Tariff headlines I know it’s tempting to move to the sidelines and delay making investments or even sell and wait and see how things develop with a view to ‘re-entering the market’ when valuations might be more attractive and the outlook clear. The problem is the evidence suggests that approach rarely works out! With new record highs being made in the US stock market last week I thought it’s worth reflecting on this.

The impact of being out of the market for a short time can be profound, as shown by this hypothetical investment in the MSCI World Index, a broad Global stock market benchmark.

- A hypothetical £1,000 investment made in 2015 turns into £3,214 for the 10-year period ending December 31, 2024.

- Miss the MSCI World’s best week, and the value shrinks to £2,940. Miss the best three months, and the total return falls to £2,498.

- There’s no proven way to time the market—targeting the best days or moving to the sidelines to avoid the worst. Staying invested and focused on the long term helps to ensure that you’re in position to capture what the market has to offer.

In GBP. For illustrative purposes. Best performance dates represent end of period (April 08, 2020, for best week; April 14, 2020, for best month; June 18, 2020, for best three months; and September 15, 2020, for best six

months). The missed best consecutive days examples assume that the hypothetical portfolio fully divested its holdings at the end of the day before the missed best consecutive days, held cash for the missed best consecutive days, and reinvested the entire portfolio in the MSCI World Index (net div., GBP) at the end of the missed best consecutive days. Data presented in the growth of £1,000 exhibit is hypothetical and assumes reinvestment of income and no transaction costs or taxes. The data is for illustrative purposes only and is not indicative of any investment. MSCI data © MSCI 2025, all rights reserved.

Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

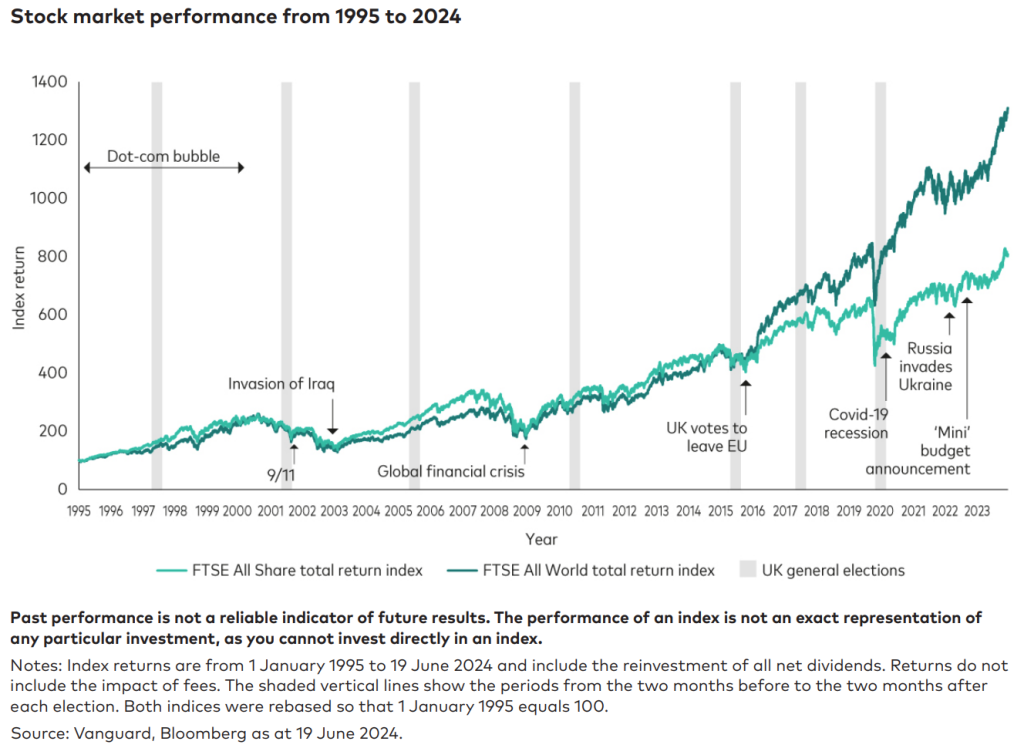

MARKET INSIGHTS: MARKETS TEND TO DISREGARD UK ELECTIONS

As we have all noticed in recent weeks elections generate lots of headlines. So it might seem like an important consideration when making investments Vanguard have analysed the performance of a balanced portfolio of 60% UK shares and 40% UK bonds between January 1987 and May 2024. During that time, there have been 10 general election periods in the UK (including the election on 4 July). They looked at portfolio performance in the period from the five months before each election to the five months after and then compared this with performance during other times and found no statistical difference in portfolio performance!

They also analysed the performance of UK and global stock markets between January 1995 and December 2023, during which period there were seven general elections. The chart below shows that the elections had a minimal impact on stock market performance.

Assessing the implications of a new government and then trying to profit by timing the market rarely works, even for seasoned professionals.

Hopefully the above illustrates that planning with your long term goals in mind, keeping perspective and being disciplined are likely far more rewarding.

Hopefully the above illustrates that planning with your long term goals in mind, keeping perspective and being disciplined are likely far more rewarding.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

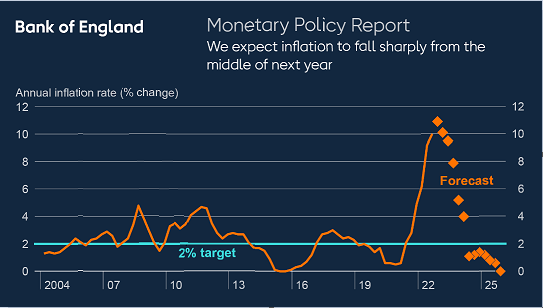

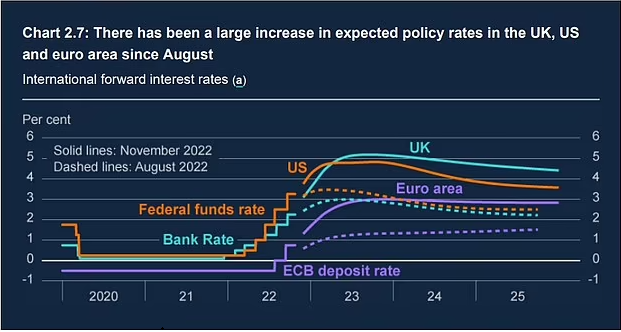

UK INFLATION AND INTERET RATE EXPECTATIONS

I am sure you are likely aware of the Bank of England increase to interest rates from 2.25% to 3% yesterday.

We are often asked about Interest rate expectations given that many of our clients have mortgages.

It may be somewhat reassuring that the Bank of England expect key measures of inflation to fall moving forward.

Here a few interesting graphs:

Source: Bank of England

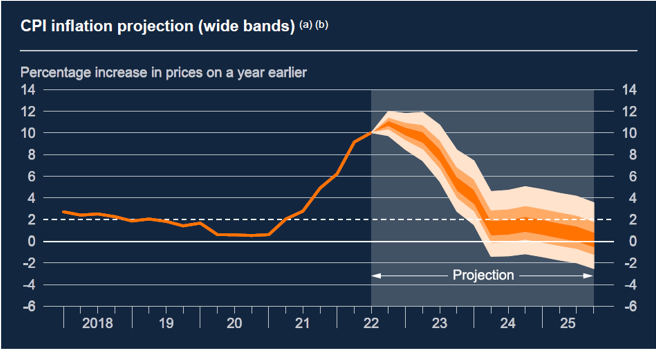

The UK is not alone in tackling inflation/interest rates

as can be seen here:

Source: Bloomberg Finance L.P. and Bank calculations

MARKET INSIGHTS: THE WEATHER IS CHANGING

The weather certainly feels like it has changed recently, hence I wanted to send an update on investment markets.

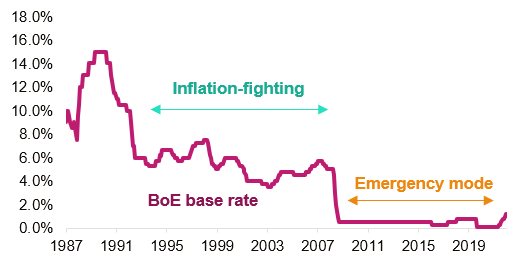

The battle against inflation has continued, Central Banks pushed through more Interest Rate hikes last month, the market barely flinched. Still firmly entrenched in Emergency Mode, interest rates will continue to rise until prices start to fall, which if course is going to have consequences for growth. A rate environment like pre-crisis is the most likely outcome, but there is going to be a fair bit of pain before we get there:

Inflation (CPI came in particularly high at 10.1%, with a 12.6% annual increase in food prices driving the reading above all estimates. This is up from 9.4% in June and marks the first time that UK prices have risen by double digits year-on-year since 1982. Given the implications this has for monetary policy, a sell-off in sterling-denominated assets followed, with the probability of a 75bp BoE interest rate hike increasing to around 30%. With further inflationary pressure expected from the energy price cap rises later this year, the outlook is left looking fragile, with the brutal squeeze on purchasing power far from over. While UK consumer confidence reading fell to a 50 year low on Friday coming in at –44, UK retail sales Ex Auto/ Fuel came in much better than expected at 0.4%.

The drought will no doubt exacerbate the problem further - farmers are finding life extremely challenging, with impending food shortage on top of ongoing energy disruption.

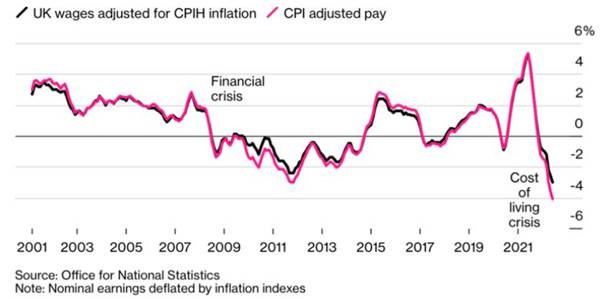

Thought this was quite a scary chart – REAL pay in the UK is falling at the fastest pace in 21 years.

Flash estimates suggested that euro zone GDP grew 3.9% year-on-year in Q2, below expectations and slightly down from the previous quarter. Inflation, on the other hand, remained persistent, with final HICP inflation at 8.9% for July as the region continues to suffer from the ramifications of Ukraine’s ongoing conflict with Russia.

In the month to July, US retail sales were unchanged, indicating that a degree of robustness remains among households. Unfortunately, the housing market is not displaying the same strength, with homebuilding squashed to the lowest level in over a year by high mortgage rates and construction material costs, muddying the country’s outlook. In line with these mixed signals, FOMC minutes were firm on inflation but acknowledged the wider economic implications of persistently aggressive policy. As a result, the committee resolved to continue hiking rates until inflation starts to decline but noted it may be appropriate for the pace of these increases to slow at some point, in order to assess their impact on the economy. This followed last week’s cooler inflation figure, which the market interpreted as a reduction in the likelihood of a 75bp September hike (measured at 40% post-release, down from around 50% before).

Equity markets are largely flat on the week while volumes remain low, having deteriorated throughout summer to the extent that movements are amplified. Earnings season is drawing to a close, with over 94% of the S&P 500 and 85% of EuroStoxx 600 now reported. Notably, although Target’s earning miss this week was not as bad as feared, following their earlier profit warning, it has renewed the focus on inventory and margin headwinds after the company was forced to slash prices to clear excess stock. As a result, it is possible that earnings estimates may need to be revised downwards in the coming months.

In China, the PBoC unexpectedly loosened monetary policy, cutting its medium-term lending rate by 10bps to 2.75% in an attempt to spur economic activity. This came after the announcement of surprisingly weak retail sales and industrial output growth as both consumer and business confidence have been depressed by COVID measures and the property market crisis. Now faced with structurally weak credit demand, evidenced by new yuan loans falling dramatically in July, policymakers are constrained by fears of stoking inflation. For now, in addition to the rate cut, Premier Li Keqiang has urged six major provinces to boost growth measures and balance COVID restrictions with economic performance whilst Chinese regulators look to guarantee bond issuance by property developers in an effort to buoy a systemically significant industry for the country.

Oil prices fell roughly 2% this week as the relatively weaker global economic outlook dampened demand while supply looks set to expand, with increased US shale production, rebounding Libyan production, and a potential nuclear agreement with Iran which would permit more oil exports.

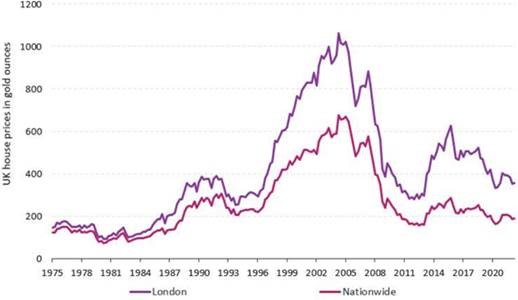

There’s been plenty in the press about slowing annual house price growth. What if you were to lot a chart showing how many ounces of gold you need to buy a house in the UK? Prices are not as lofty as you might think in those terms.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

MARKET INSIGHTS: MORE UNIQUE AND COMPELLING OPPORTUNITIES THAN SEEN IN YEARS

Markets have begun plotting a path to recovery. Yet, the economy is in a dire state with significant uncertainty.

We work with you and the best investment management teams to achieve your objectives.

Hear directly from Morningstar who explain where they see opportunities ahead.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

FINANCIAL RESOLUTIONS

WELCOME TO 2020! WHAT ARE YOUR PLANS FOR THE NEW DECADE

What does Wealth look like to you?

We all have different goals and aspirations in life

EVEN THE SMARTEST PEOPLE GET IT GROSSLY WRONG

As you are undoubtedly aware, the U.K. election has been announced for December 12th. This is likely to be the biggest—perhaps only—talking point between now and Christmas, so I wanted to offer some substance behind our actions (or in this case, inactions).

Let us be clear, while these are uncharted waters, political uncertainty is nothing new. On this occasion, as in the past, people will jump over themselves to tell you the “right way”. Whether we are judging the merits of the candidates or working through our investment positioning, we must favour research over reaction and urge all our clients to do the same.

Chief among these is the temptation to react too quickly or with too much confidence in the lead up to the outcome of this significant event.

If you are cynical of this stance, I share the below quotes from the U.S. election and Brexit referendum, where even the smartest of people got it grossly wrong.

> Incorrect U.S. Election Predictions (U.S. stocks rallied 2.22% on the day after the election and around 9% in the three months following)

“We would expect a small global stock market rally if Clinton wins (about 2 percent) and a large decline if Trump wins (about 10 percent)”. Eric Zitzewitz, Professor of Economics at Dartmouth College

“The S&P 500 will fall by 3% to 5% immediately if Trump is elected”. Tobias Levkovich, Citigroup's chief U.S. equity analyst

“If investors are wrong and Trump wins, we should expect a big markdown in expected future earnings for a wide range of stocks – and a likely crash in the broader market.” Simon Johnson, professor at MIT Sloan and former chief economist of the IMF

> Incorrect Brexit Referendum Predictions (U.K. stocks fell 3.15% the day after the referendum but gained around 13% in the six months following. Economic growth also continued to rise)

“A vote to leave would tip our economy into year-long recession with at least 500,000 UK jobs lost”. George Osborne, served as Chancellor of the Exchequer under Prime Minister David Cameron

“Leaving Europe would tip the country into recession”. David Cameron, ex-Prime Minister UK

“Brexit would trigger recession”, predicted -0.3% GDP for Q3”. IMF Forecasts

“Short term impact of -1.25% GDP”. OECD Forecasts

“It would be likely to have a negative impact in the short term… I certainly think that would increase the risk of recession”. Mark Carney, Bank of England

> What about a Corbyn government?

Political biases aside, two of the widely quoted risks to investors seems to be in a Corbyn government or a hung parliament. It is easy to build an ugly bear case—no matter which scenario you look at—and we are mindful that the media will take full advantage of this fear-driven sentiment (they want to sell newspapers after all). We urge investors to keep a level head, and while these issues have substance, investors should look through media exaggeration as political risk is largely unpredictable.

It is for circumstances like this that we take a diversified approach. We don’t go “all in” on a given outcome, because we can limit the risks by spreading your eggs across multiple baskets. We have global exposure, defensive exposure and different currencies, to name a few, which would all help buffer any election risks.

Last, we leave you with a few key points.

1. The key question on many investors lips is whether they should sell, hold or buy. To our eye, the answer is simple… manage risks, stay informed and—if in doubt—stay the course.

2. Any turbulence in markets may create great opportunities to purchase assets that will add meaningfully to returns in the future. We are not there yet, but we will look at this opportunistically.

3. We appreciate that the current period is very unsettling for investors and will cause debate among your families. We will do our utmost to support our clients during this time.

PRIME MINISTER THERESA MAY'S DEPARTURE

SOME SCENARIOS FROM UBS