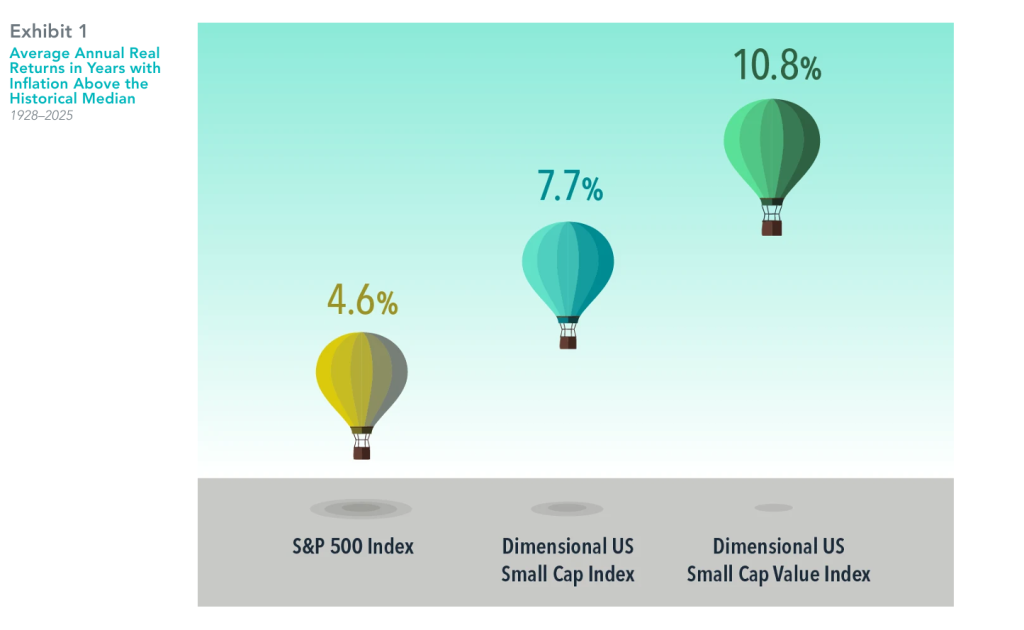

Outpacing Inflation with Stocks

Inflation is back in the news of late, as the year-over-year change in the consumer price index is at the highest level since 2023 in the US which is the worlds largest economy. This may stoke fears of further inflation for many investors.

It’s important to note that expected inflation is incorporated into the expected returns demanded by market participants. To the extent inflation is expected to impact either future cash flows from an investment, or the discount rate applied to these cash flows, market prices adjust to compensate, resulting in positive expected real returns. This is borne out in historical data. Average real returns for the broad US stock market, based on the S&P 500 Index, have been positive even in years when US inflation was above the historical median. Average real returns for US small cap and small cap value stocks have been even higher, implying investors should not shy away from tilting toward higher expected return stocks even if inflation expectations are elevated.

We believe one way for investors to deal with inflation is to outpace it. Stocks have been a good way to do this historically, as the evidence from the US illustrates.

To review the diversification of your own investments feel free to get in touch.

In USD. US inflation is the annual rate of change in the consumer price index for all urban consumers (CPI-U, not seasonally adjusted) from the US Bureau of Labor Statistics. Nominal return is the rate of return on an investment without adjusting for inflation. Real return is the rate of return on an investment after adjusting for inflation. Real returns are calculated using the following method: [(1 + nominal return) / (1 + inflation rate)] – 1. The Dimensional indices represent academic concepts that may be used in portfolio construction and are not available for direct investment or for use as a benchmark. Index returns are not representative of actual portfolios and do not reflect costs and fees associated with an actual investment.

See “Index Descriptions” in the appendix for descriptions of the Dimensional index data.

S&P data © 2026 S&P Dow Jones Indices LLC, a division of S&P Global. Indices are not available for direct investment.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

Quarterly Market Review

1st Quarter 2026

1st Quarter 2026

This report takes into account the energy crisis that started unravelling in early March 2026. If you want to compare returns in Emerging markets/ Value / Growth or Smaller companies in the period please see attached for the numbers together with information on interest rates.

This is also evidence that maintaining well-diversified, long-term thinking in your investment approach rather than reacting to short term news about wars and the oil price is essential.

We are here to help you develop and monitor carefully considered plans to meet your life objectives for the future which is probably more important to you.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

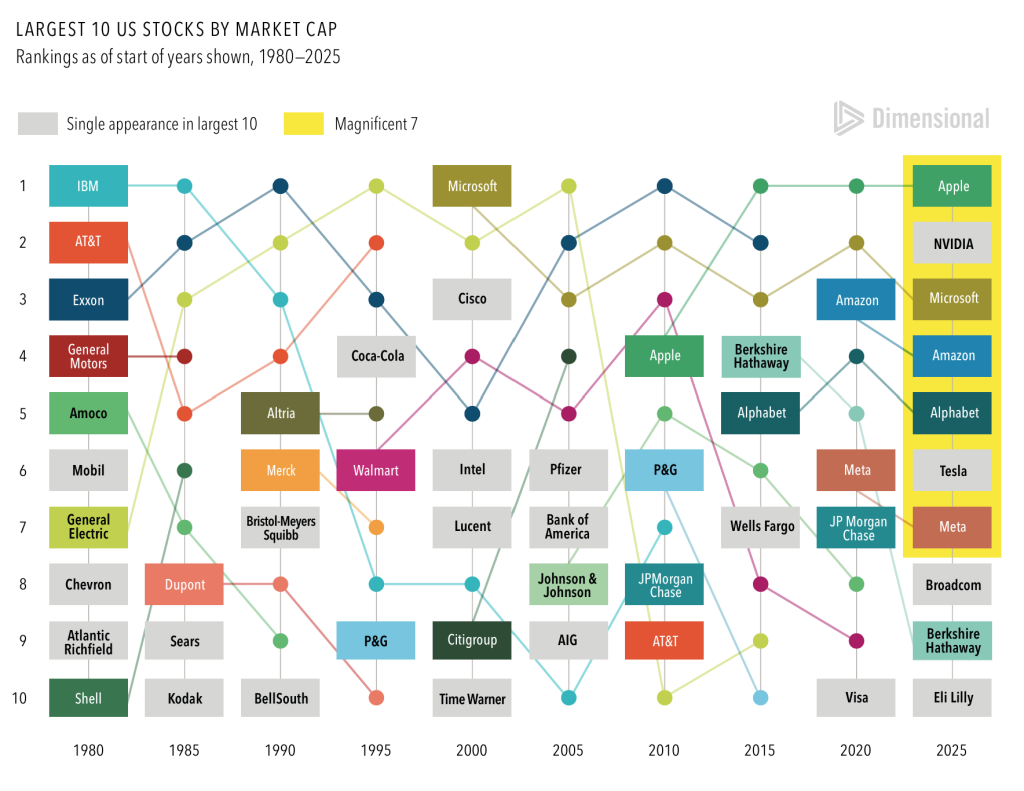

Will the Magnificent 7 Stay on Top

The Magnificent 7 entered 2025 among the Top 10 largest US stocks. But before making an outsize bet on gains from these technology giants, investors should consider a few lessons from market history.

- It’s hard to stay on top. For example, only three of the 10 biggest companies from 1980 made the 2000 list—and none of them was in 2025’s Top 10.

- Industries ebb and flow. Technology-focused firms currently dominate the list. But in 1980, six of the 10 largest companies were in the energy sector.

- New technology doesn’t benefit only tech firms. Throughout history, companies across industries have used technology to innovate and grow.

Diversification enables investors to share in the success of today’s top companies while staying positioned to benefit from tomorrow’s market leaders.

The Magnificent 7 stocks are Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla.

Source: Dimensional, using data from the Center for Research in Security Prices and Compustat. Includes all US common stocks. Largest stocks identified at the end of the calendar year preceding the respective period by sorting eligible US stocks on market capitalisation using data provided by the CRSP, University of Chicago.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

Key steps to take before the tax year ends

With the 2025/26 tax year-end approaching, now is the time to act to maximise your financial opportunities. Key priorities include using your £20,000 ISA allowance for tax-efficient growth and contributing up to £60,000 (or more if carry forward is available and relevant earnings are sufficient) to your pension to take advantage of tax relief and long-term benefits. Other allowances, such as Capital Gains Tax, Dividend Allowance and Junior ISAs, are ‘use it or lose it’ opportunities. On page 08, we explain why early action avoids last-minute stress, secures tax savings and ensures financial growth.

With rising life expectancy, more of us will need long-term care, making early financial planning essential. Fees have surged, and regional cost disparities add to the challenge. Funding options include annuities, insurance, investments and equity release. On page 12, we consider how professional advice is crucial for navigating tax implications and securing a sustainable plan for future care needs.

Inheriting wealth can be life-changing but comes with challenges. On page 28, we explain why holding excessive cash may not be the best choice as inflation erodes its value. Instead, consider diversified investments to foster growth. Align your strategies with your goals, whether it’s retirement or supporting your family, and seek professional advice to maximise tax benefits and avoid pitfalls.

Financial uncertainty is growing, with many feeling life is unpredictable. Rising inflation, energy costs, and tax increases fuel concerns, prompting shifts such as increased cash savings and delayed retirements. While saving is important, balancing short-term needs with long-term investments is key. Reviewing pensions and seeking advice builds resilience and confidence. Turn to page 06.

A complete list of the articles featured in this issue appears opposite page and on page 03.

Wealth planning for your future

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

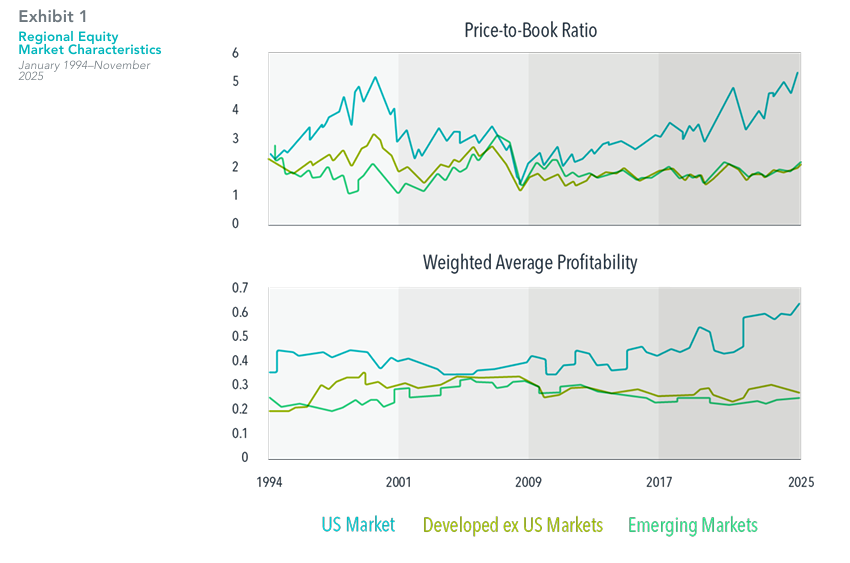

US Market Not Partying Like It’s 1999

Much has been made of current US stock market valuations. As of November 30, the aggregate price-to-book ratio of the US market was 5.21—more than double the valuations of non-US developed and emerging market stocks. Many observers have drawn parallels to the late 1990s, when the gap between US and non-US valuations was similarly wide. Some view this as an omen for future returns—and not a good one given the US market’s infamous “lost decade” starting in 2000.

But this comparison may not be apples to apples. The weighted average profitability of the US market has surged in recent years, rising from 42% five years ago to 62% as of November 30. That’s a very different backdrop from 1999, when US market profitability declined over the subsequent five years.

Valuation ratios can be high because expected returns are low or because expected future earnings growth is high. There is no evidence that investors can reliably disentangle these effects in real time. But the strong profitability growth of recent years suggests a more nuanced story behind today’s US valuations. It is not clear that the US market requires poor future returns in order to “grow into” its current valuation levels.

In USD. Source: CRSP and Compustat data calculated by Dimensional. Fama/French data provided by Fama/French. US Market is represented by the Fama/French Total US Market Research Index. Developed ex US Market is represented by the Fama/French International Market Research Index. Emerging Markets is represented by the Fama/French Emerging Markets Index. Monthly aggregate price-to-book ratios are computed as the inverse of the weighted average book-to-market value as of month-end. Firms with negative book value are excluded. Book-to-market ratios above 10 are winsorized as the cutoff value in non-US markets. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. Profitability values above 5 and below −2 are winsorized as the cutoff value. The Fama/French indices represent academic concepts that may be used in portfolio construction and are not available for direct investment or for use as a benchmark. Eugene Fama and Ken French are members of the Board of Directors of the general partner of, and provide consulting services to, Dimensional Fund Advisors LP.

Aggregate price-to-book ratio: The ratio of a firm’s market value to its book value, where market value is computed as price multiplied by shares outstanding, and book value is the value of stockholder equity as reported on a company’s balance sheet.

Profitability: A company’s operating income before depreciation and amortization minus interest expense scaled by book equity.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

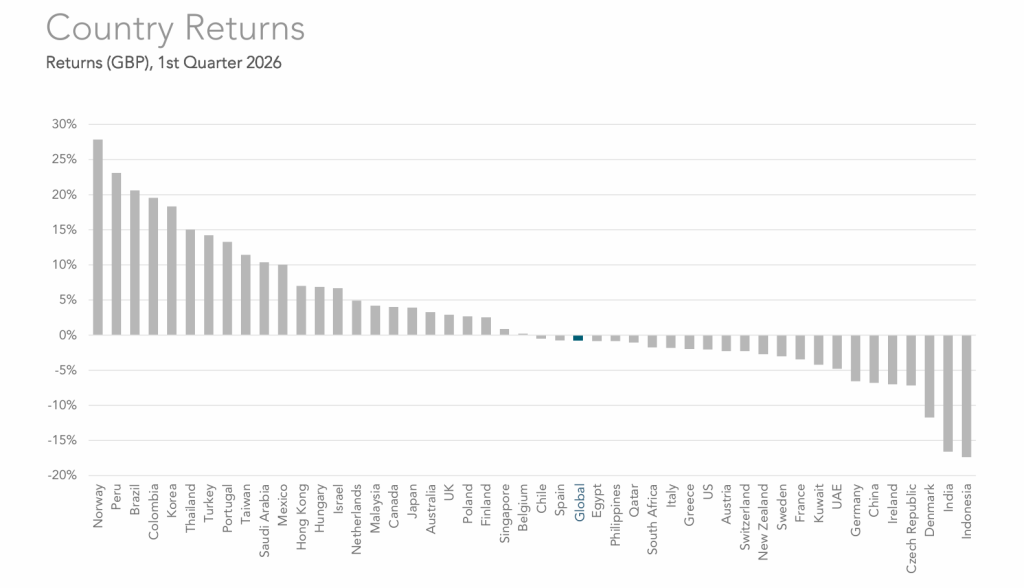

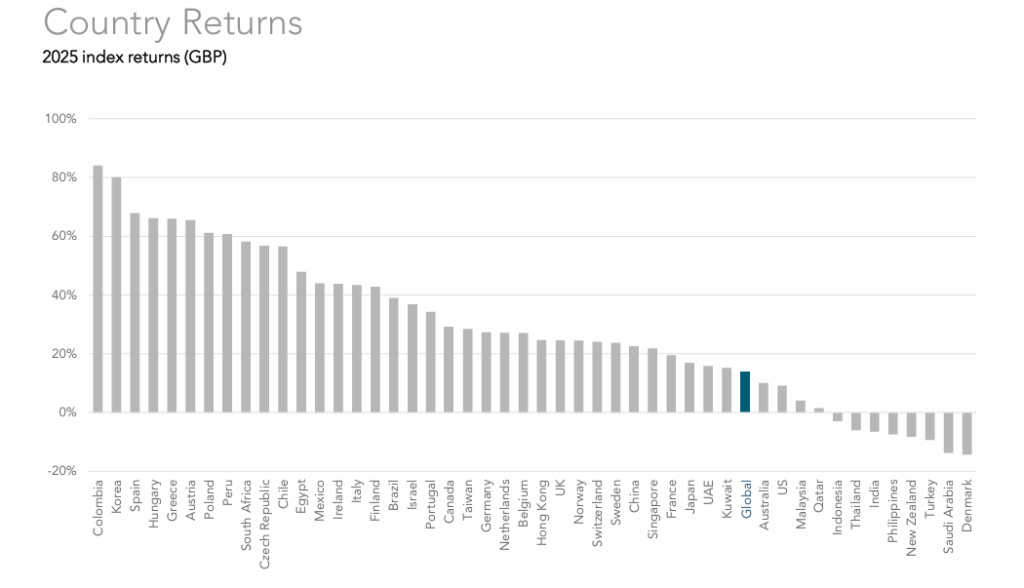

Annual Market Review 2025

So in the end after all the uncertainty (Trump's trade tariffs in April and the shift in US Trade Policy among other developments) let's look at 2025. Most investors are much better off than those sitting in cash on deposit. If you want to know which countries returns were higher and was it Emerging markets/ Value / Growth or Smaller companies that performed better in the period please see attached for the answers together with information on interest rates.

This is also evidence that maintaining well-diversified, long-term thinking in your investment approach rather than reacting to short term valuations is essential. As it happened you would have been better off buying the dip in valuations in April!

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

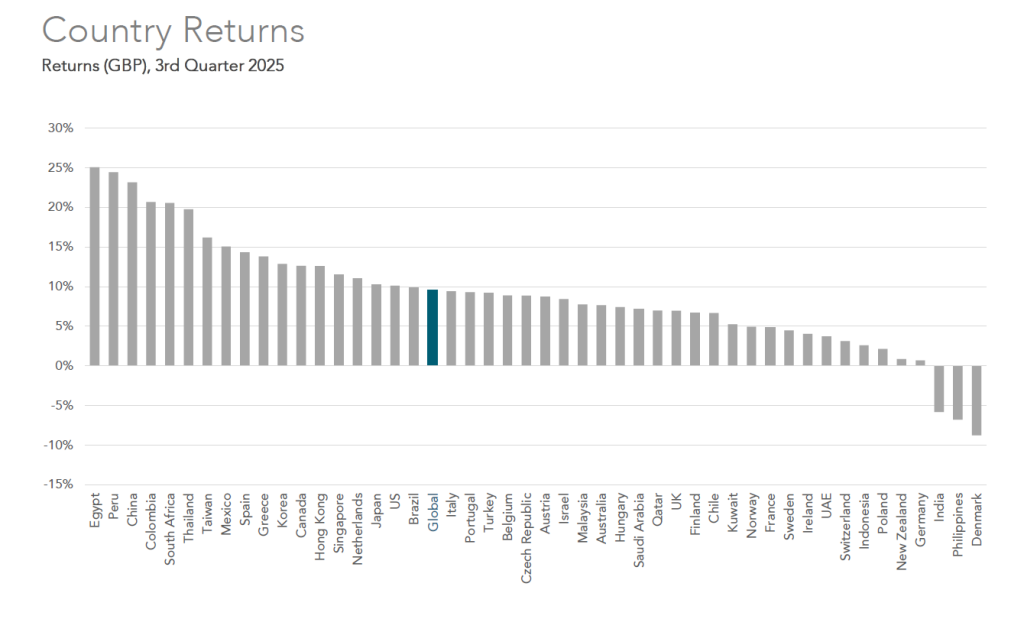

Quarterly Market Review

3rd Quarter 2025

3rd Quarter 2025

Here's a breakdown of what happened last quarter. This is for those of you interested in aspects such as which countries returns were higher and whether it was Value / Growth or Smaller companies that performed better in the period.

This is also evidence that maintaining well-diversified, long-term thinking in your investment approach rather than reacting to short term valuations is key. We can help you develop and monitor carefully considered plans to meet your life objectives for the future which is probably more important to you.

Happy Diwali!

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

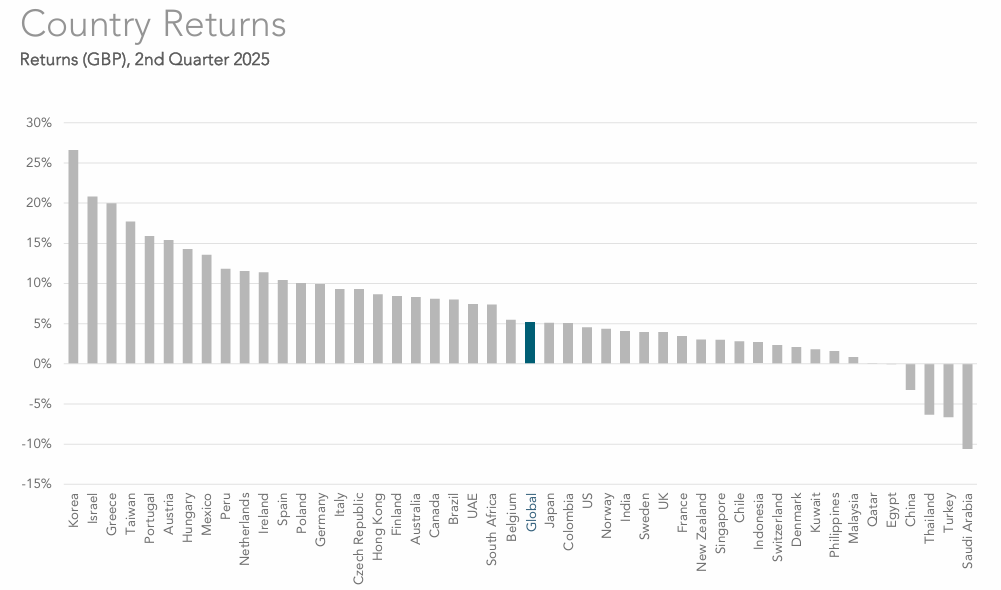

Quarterly Market Review

2nd Quarter 2025

2nd Quarter 2025

Here's a breakdown of what happened last quarter. This is for those of you interested in aspects such as which countries returns were higher (Korea!) or whether Value / Large or Smaller companies performed better in the period. There is also a Long-Term Market Summary and Average Quarterly Returns for Stocks and Bonds going back 20 years!

This should provide comfort that maintaining a well-diversified investment approach, rather than making predictions about what will come next, is more reliable for your savings.

With this in mind we help develop carefully considered financial plans to achieve your life objectives for the future which is probably what matters more to you!

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

Market Insight: Sweeping changes

Welcome to our latest issue. The October 2024 Budget proposed sweeping changes to Inheritance Tax (IHT), significantly tightening the laws that were previously more forgiving for families with trading businesses and farmland. Effective from April 2026, these types of assets will now incur IHT at a reduced rate of 20% on valuations exceeding £1 million. On page 04, we consider why the changes are leaving many families scrambling to reassess their estate planning strategies.

Ten years ago, pension freedoms revolutionised how people access their retirement savings. These changes offered savers over 55 greater options to withdraw and manage their pension pots. However, a decade later, research indicates that many individuals are making critical financial decisions without seeking advice or fully understanding the tax implications. Read the full article on page 03.

A complete list of the articles featured in this issue appears on page 02.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

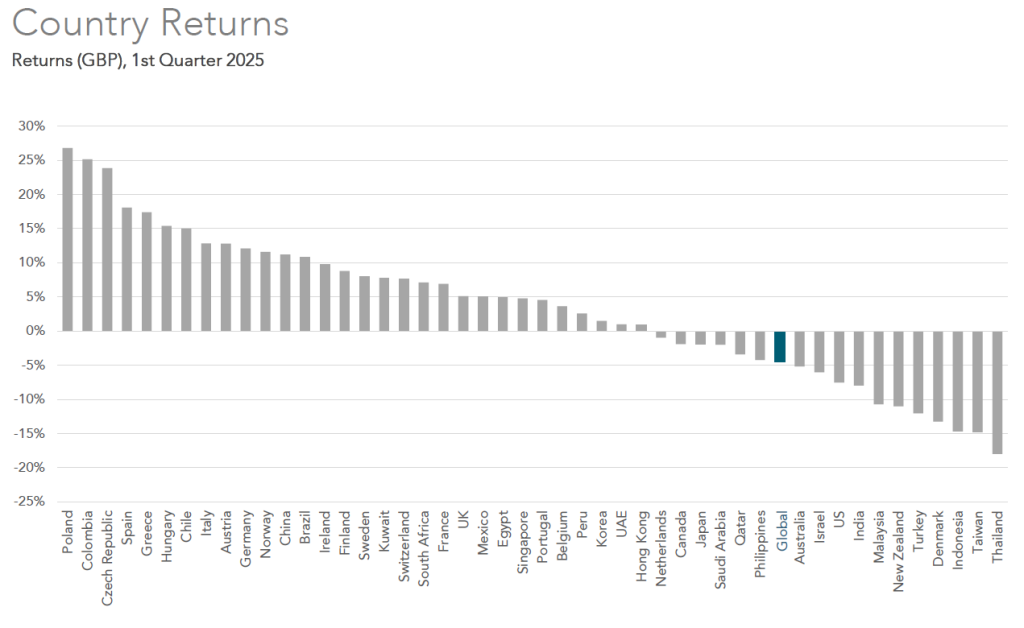

Quarterly Market Review

1st quarter 2025

Here's a breakdown of what happened last quarter. This is for those of you interested in aspects such as which countries returns were higher or whether Value / Growth or Smaller companies performed better in the period. I am aware that there have been many movements since April however for the purpose of completeness this covers the first quarter of the year.

This is also evidence that maintaining well-diversified, long-term thinking in your investment approach rather than reacting to daily valuations is key. We can help you develop and monitor carefully considered plans to meet your life objectives for the future which is probably more important to you!

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below