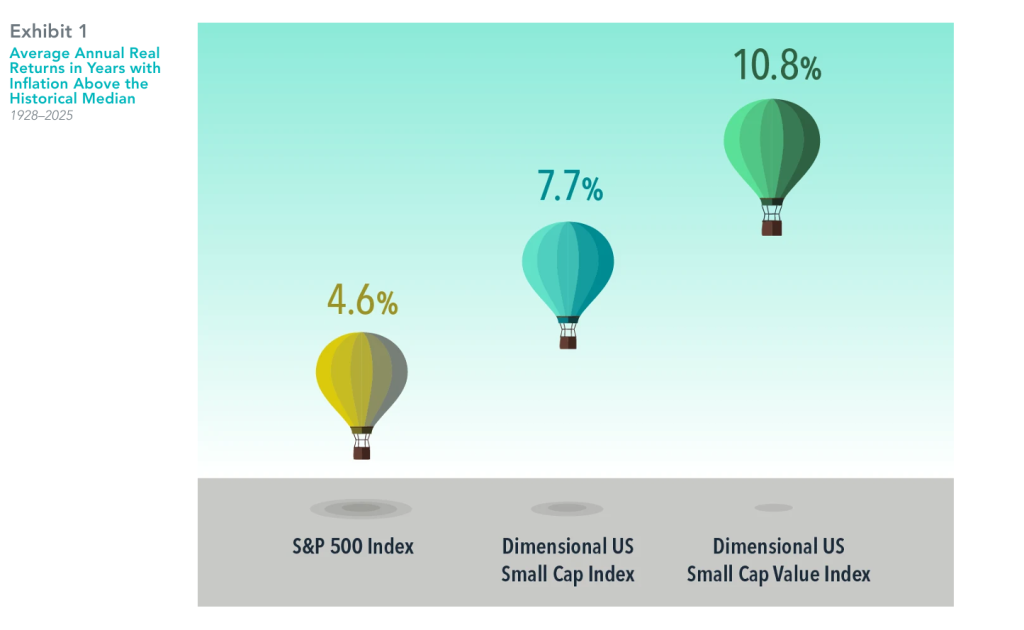

Outpacing Inflation with Stocks

Inflation is back in the news of late, as the year-over-year change in the consumer price index is at the highest level since 2023 in the US which is the worlds largest economy. This may stoke fears of further inflation for many investors.

It’s important to note that expected inflation is incorporated into the expected returns demanded by market participants. To the extent inflation is expected to impact either future cash flows from an investment, or the discount rate applied to these cash flows, market prices adjust to compensate, resulting in positive expected real returns. This is borne out in historical data. Average real returns for the broad US stock market, based on the S&P 500 Index, have been positive even in years when US inflation was above the historical median. Average real returns for US small cap and small cap value stocks have been even higher, implying investors should not shy away from tilting toward higher expected return stocks even if inflation expectations are elevated.

We believe one way for investors to deal with inflation is to outpace it. Stocks have been a good way to do this historically, as the evidence from the US illustrates.

To review the diversification of your own investments feel free to get in touch.

In USD. US inflation is the annual rate of change in the consumer price index for all urban consumers (CPI-U, not seasonally adjusted) from the US Bureau of Labor Statistics. Nominal return is the rate of return on an investment without adjusting for inflation. Real return is the rate of return on an investment after adjusting for inflation. Real returns are calculated using the following method: [(1 + nominal return) / (1 + inflation rate)] – 1. The Dimensional indices represent academic concepts that may be used in portfolio construction and are not available for direct investment or for use as a benchmark. Index returns are not representative of actual portfolios and do not reflect costs and fees associated with an actual investment.

See “Index Descriptions” in the appendix for descriptions of the Dimensional index data.

S&P data © 2026 S&P Dow Jones Indices LLC, a division of S&P Global. Indices are not available for direct investment.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

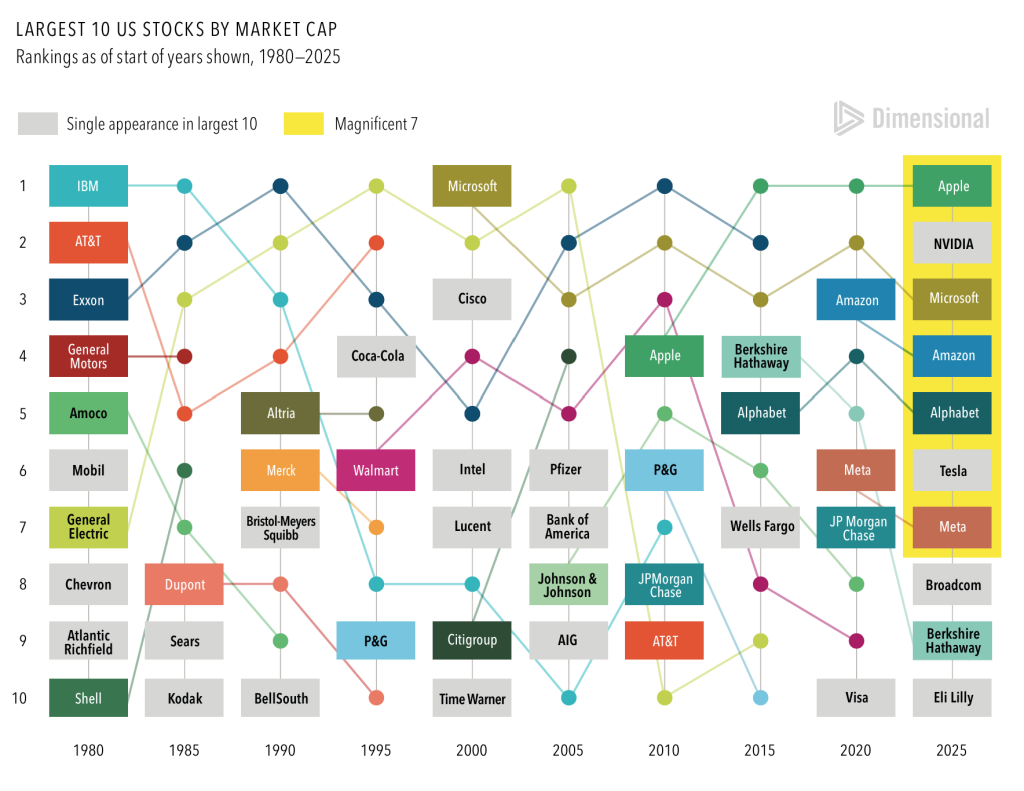

Will the Magnificent 7 Stay on Top

The Magnificent 7 entered 2025 among the Top 10 largest US stocks. But before making an outsize bet on gains from these technology giants, investors should consider a few lessons from market history.

- It’s hard to stay on top. For example, only three of the 10 biggest companies from 1980 made the 2000 list—and none of them was in 2025’s Top 10.

- Industries ebb and flow. Technology-focused firms currently dominate the list. But in 1980, six of the 10 largest companies were in the energy sector.

- New technology doesn’t benefit only tech firms. Throughout history, companies across industries have used technology to innovate and grow.

Diversification enables investors to share in the success of today’s top companies while staying positioned to benefit from tomorrow’s market leaders.

The Magnificent 7 stocks are Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla.

Source: Dimensional, using data from the Center for Research in Security Prices and Compustat. Includes all US common stocks. Largest stocks identified at the end of the calendar year preceding the respective period by sorting eligible US stocks on market capitalisation using data provided by the CRSP, University of Chicago.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

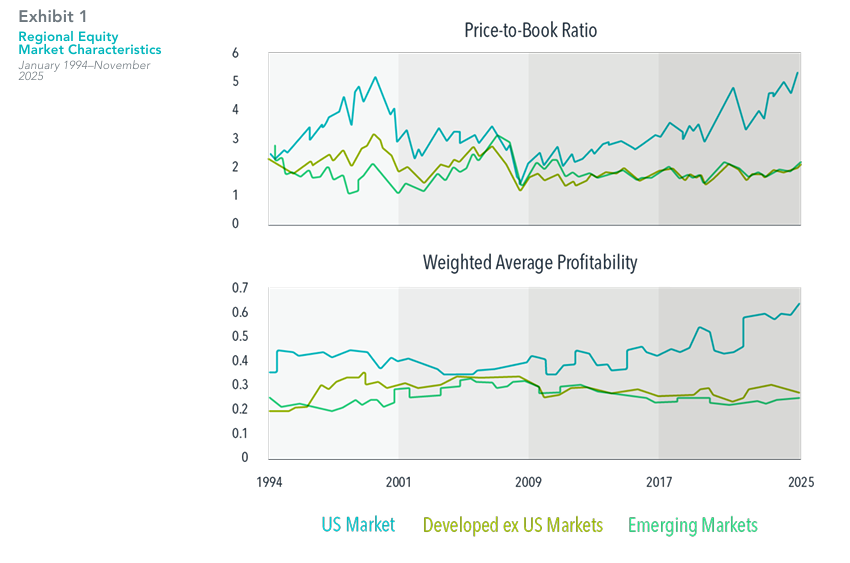

US Market Not Partying Like It’s 1999

Much has been made of current US stock market valuations. As of November 30, the aggregate price-to-book ratio of the US market was 5.21—more than double the valuations of non-US developed and emerging market stocks. Many observers have drawn parallels to the late 1990s, when the gap between US and non-US valuations was similarly wide. Some view this as an omen for future returns—and not a good one given the US market’s infamous “lost decade” starting in 2000.

But this comparison may not be apples to apples. The weighted average profitability of the US market has surged in recent years, rising from 42% five years ago to 62% as of November 30. That’s a very different backdrop from 1999, when US market profitability declined over the subsequent five years.

Valuation ratios can be high because expected returns are low or because expected future earnings growth is high. There is no evidence that investors can reliably disentangle these effects in real time. But the strong profitability growth of recent years suggests a more nuanced story behind today’s US valuations. It is not clear that the US market requires poor future returns in order to “grow into” its current valuation levels.

In USD. Source: CRSP and Compustat data calculated by Dimensional. Fama/French data provided by Fama/French. US Market is represented by the Fama/French Total US Market Research Index. Developed ex US Market is represented by the Fama/French International Market Research Index. Emerging Markets is represented by the Fama/French Emerging Markets Index. Monthly aggregate price-to-book ratios are computed as the inverse of the weighted average book-to-market value as of month-end. Firms with negative book value are excluded. Book-to-market ratios above 10 are winsorized as the cutoff value in non-US markets. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. Profitability values above 5 and below −2 are winsorized as the cutoff value. The Fama/French indices represent academic concepts that may be used in portfolio construction and are not available for direct investment or for use as a benchmark. Eugene Fama and Ken French are members of the Board of Directors of the general partner of, and provide consulting services to, Dimensional Fund Advisors LP.

Aggregate price-to-book ratio: The ratio of a firm’s market value to its book value, where market value is computed as price multiplied by shares outstanding, and book value is the value of stockholder equity as reported on a company’s balance sheet.

Profitability: A company’s operating income before depreciation and amortization minus interest expense scaled by book equity.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

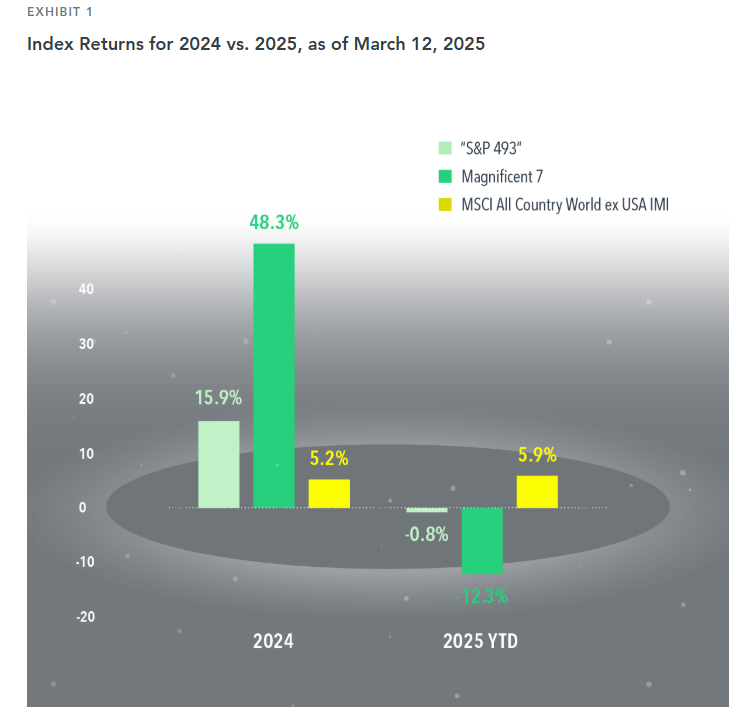

Chasing the returns of the biggest stocks in the US?

If top stocks exert a gravitational pull on the broad market’s return, the Magnificent 7 (Apple, Nvidia, Amazon, Tesla, Meta, Microsoft, Alphabet)have acted like the TON 618 black hole over the US the past few years.1 Accounting for about one-third of the S&P 500 Index’s weight2, the performance of these stocks has been a big driver of market-capitalization-weighted US large cap stock index returns.

This force can pull in a positive or negative direction. In 2024, the S&P 500 returned 25.0%. This was driven heavily by the Magnificent 7, which returned 48.3%. The other 493 stocks in the index collectively returned 15.9%. This year, the opposite effect has played out: The Magnificent 7 returned –12.3% through March 12, compared to –0.8% for the “S&P 493.”

The swings in performance for a US large cap index make a compelling case for global all cap diversification, which helps lessen exposure to the Magnificent 7. While non-US stocks underperformed the US in 2024, the MSCI All Country World ex USA IMI Index is outpacing the US thus far in 2025. Diversifying across regions and market capitalization is one way to mitigate the impact of a handful of stocks.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below

MARKET INSIGHTS: THE VALUE OF STOCKS AROUND THE WORLD

This infographic seems to be a favourite at client meetings as not many people have seen the World Equity Market Capitalisation presented in this way. This was as at the end of December 2023 where Apple represented 4% of valuations which is quite astonishing when you see that the value of the UK is only c. 4%.

It’s clear the US is the biggest market in the world and why a diversified investment approach taking these weightings into account makes sense.

(Click on image above to zoom)

Source: Dimensional. GBP. Market cap data is free-float adjusted and meets minimum liquidity and listing requirements. Dimensional makes case-by-case determinations about the suitability of investing in each emerging market, making considerations that include local market accessibility, government stability and property rights before making investments. China A-shares that are available for foreign investors through the Hong Kong Stock Connect program are included in China. 30% foreign ownership limit and 25% inclusion factor are applied to China A-shares. Many nations not displayed. Totals may not equal 100% due to rounding. For educational purposes; should not be used as investment advice. Bloomberg data provided by Bloomberg. Diversification neither assures a profit nor guarantees against loss in a declining market.

Risks : Buying Investments can involve risk. The value of your Investments and the income from them can go down as well as up and is not guaranteed at anytime. You may not get back the full amount you invested. Information on past performance is not a reliable indicator for future performance. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it.

To discuss your financial requirements or obtain other information click below

Share this article with your friends by clicking below